[ad_1]

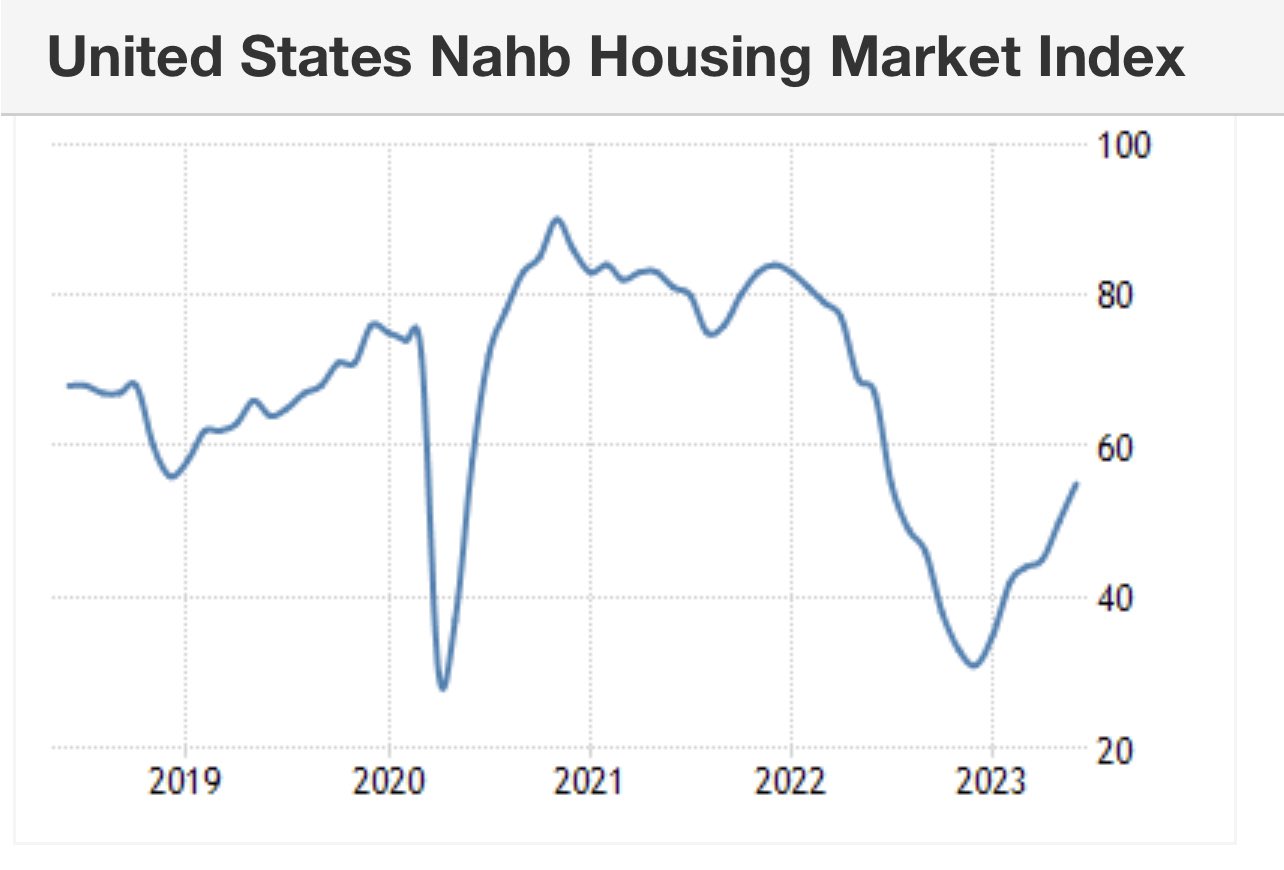

The builders confidence index came out yesterday and it’s all smiles lately, as the builders believe they can sell more homes. Historically speaking, the key level for builders confidence is 50: Anything below 50 is a recession and anything above 50 is an expansion. As you can see below, we broke over 50 yesterday as the index came in at 55.

Tuesday’s massive housing starts print will get revised lower, but the trend for the homebuilders, new home sales, and builders’ confidence has been intact since November of 2022.

Let’s look at the housing starts data and make sense of it all.

From Census: Housing starts: Privately‐owned housing starts in May were at a seasonally adjusted annual rate of 1,631,000. This is 21.7 percent (±14.8 percent) above the revised April estimate of 1,340,000 and is 5.7 percent (±10.8 percent)* above the May 2022 rate of 1,543,000. Single‐family housing starts in May were at a rate of 997,000; this is 18.5 percent (±14.1 percent) above the revised April figure of 841,000. The May rate for units in buildings with five units or more was 624,000.

This was an extreme month-to-month print on housing starts. It is likely to be revised lower as this has always been the case with really big housing starts prints — both positive and negative. It was a such a shocking print that a few economic bears kicked their recession call out to 2024 because housing is traditionally a leading economic indicator.

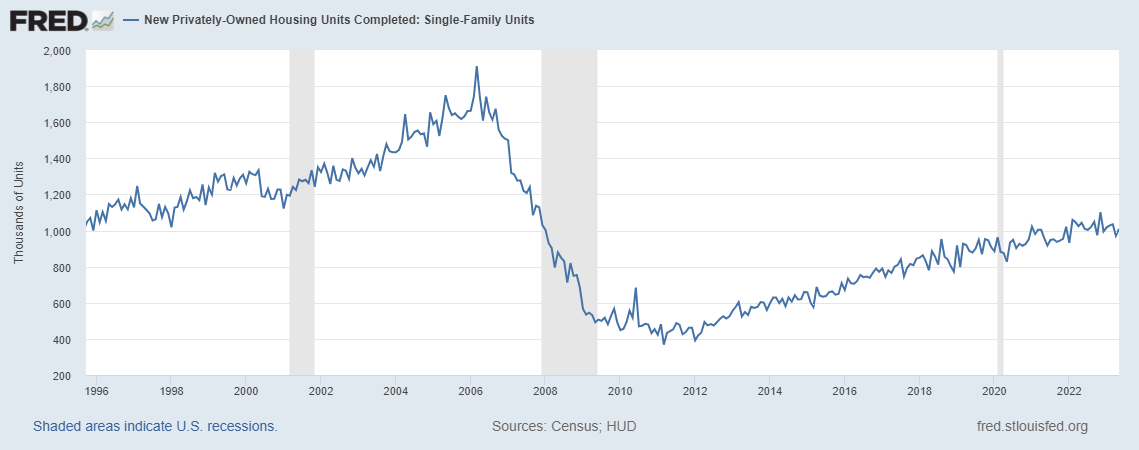

Housing Completions: Privately‐owned housing completions in May were at a seasonally adjusted annual rate of 1,518,000. This is 9.5 percent (±12.3 percent)* above the revised April estimate of 1,386,000 and is 5.0 percent (±13.0 percent)* above the May 2022 rate of 1,446,000. Single‐family housing completions in May were at a rate of 1,009,000; this is 3.9 percent (±13.9 percent)* above the revised April rate of 971,000. The May rate for units in buildings with five units or more was 493,000.

Housing completion data is still the saddest housing data line we have, but it also shows how different the housing market is now versus when housing crashed in 2008. Housing completions have been prolonged and still need to be faster: As you can see in the chart below, we haven’t gone anywhere for some time.

Unlike the housing bubble years when starts, permits, and completions were moving up and down, this time the lagging caused by COVID-19 delays is evident. However, we are past COVID-19 time, and this data line is still slower than my tortoise Grundy.

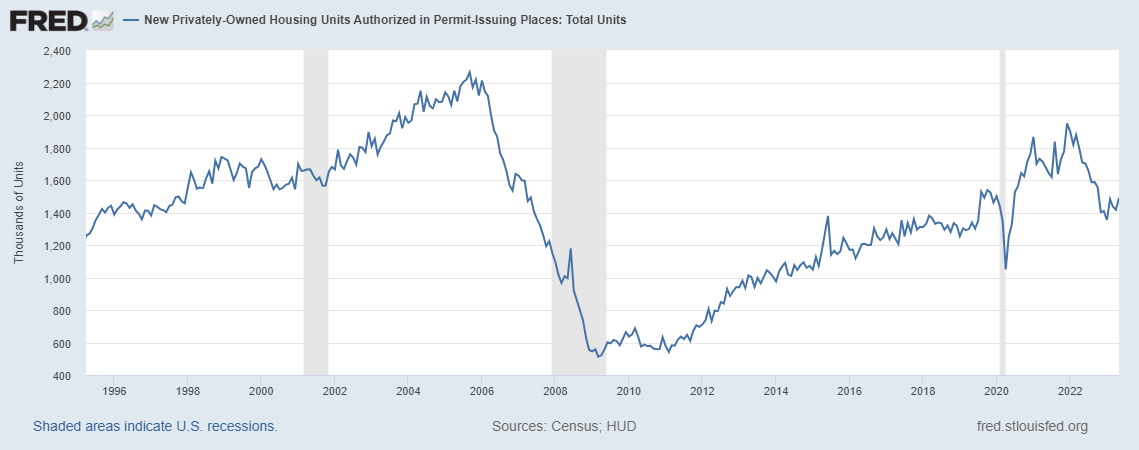

Building Permits: Privately‐owned housing units authorized by building permits in May were at a seasonally adjusted annual rate of 1,491,000. This is 5.2 percent above the revised April rate of 1,417,000, but is 12.7 percent below the May 2022 rate of 1,708,000. Single‐family authorizations in May were at a rate of 897,000; this is 4.8 percent above the revised April figure of 856,000. Authorizations of units in buildings with five units or more were at a rate of 542,000 in May.

The missing link to ending the housing recession is housing permits. Traditionally in all expansions, housing permits are rising wildly when builders’ confidence is bouncing hard off the bottom. Permits just haven’t gotten there yet, and for a good reason. First, as you can see below, housing permits have stabilized for sure but haven’t taken off yet.

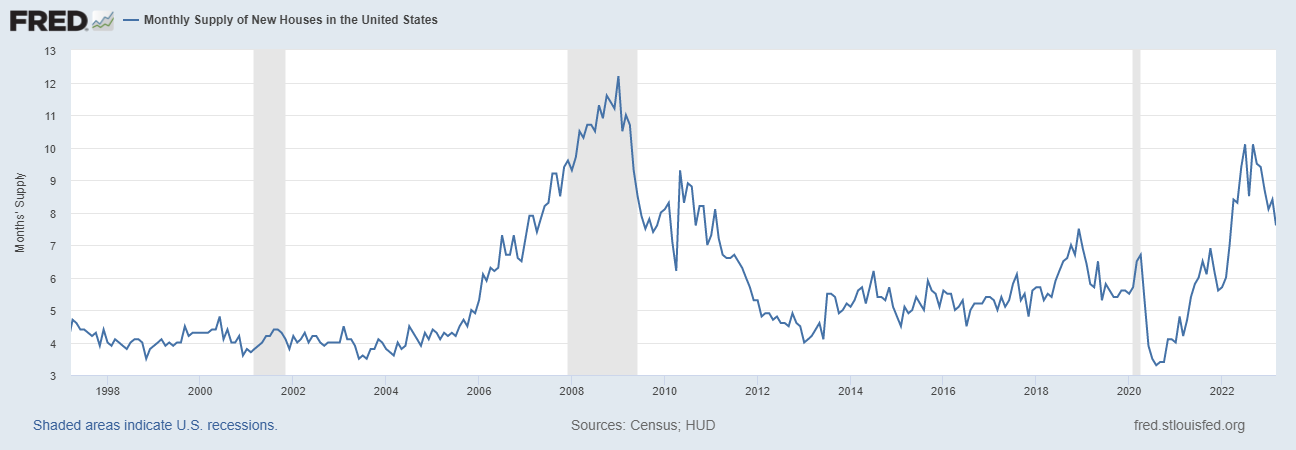

I have a straightforward model for when the homebuilders will start issuing new permits with some kick. My rule of thumb for anticipating builder behavior is based on the three-month supply average. This has nothing to do with the existing home sales market — this monthly supply data only applies to the new home sales market, and the current 7.6 months are too high for the builders to issue new permits with any kick and duration.

- When supply is 4.3 months and below, this is an excellent market for builders.

- When supply is 4.4-6.4 months, this is just an OK market for builders. They will build as long as new home sales are growing.

- When the supply is 6.5 months and above, the builders will pull back on construction.

As you can see below, builders have made good progress getting the monthly supply down, but they are just not able to get a strong push on permits yet, as they are still working off their backlog. Some of those homes haven’t even started construction yet.

Many people use housing as a leading indicator of the U.S. going in and out of a recession. As you can imagine, with the builders’ confidence rising so much and now housing starts with a giant print, some are beginning to question their recession call for 2023.

For me, it’s all about permits and demand growth, and we are working our way back to normal for this sector, we’re just not there yet. Can you imagine a housing market with mortgage rates at 5% instead of 7%? A lot of housing data would firm up more with lower mortgage rates.

The builders have some significant advantages in selling their homes because they sell them as a commodity and don’t have to deal with some of the issues that the traditional home seller has to deal with. In a high mortgage rate environment, they can offer lower rates and peel off some buyers who would generally go into the existing home sales market.

All in all, this was a shocking report on the headline. However, when you dig a bit deeper, it shows the positive housing trend that started in November of 2022 continues, but more work needs to be done.

[ad_2]

Source_link